Traditional Bank Loans

Banks are the largest business lenders and probably the first place you think about when getting a small business loan. Bank loans some of the lowest cost loans available, but it can be difficult to qualify. About 72% of small business owners who apply get rejected. Banks usually require strong personal and/or business credit scores, a personal guarantee, collateral, and healthy financials. Applying also takes serious effort and time. The whole process lasts about one to three months.

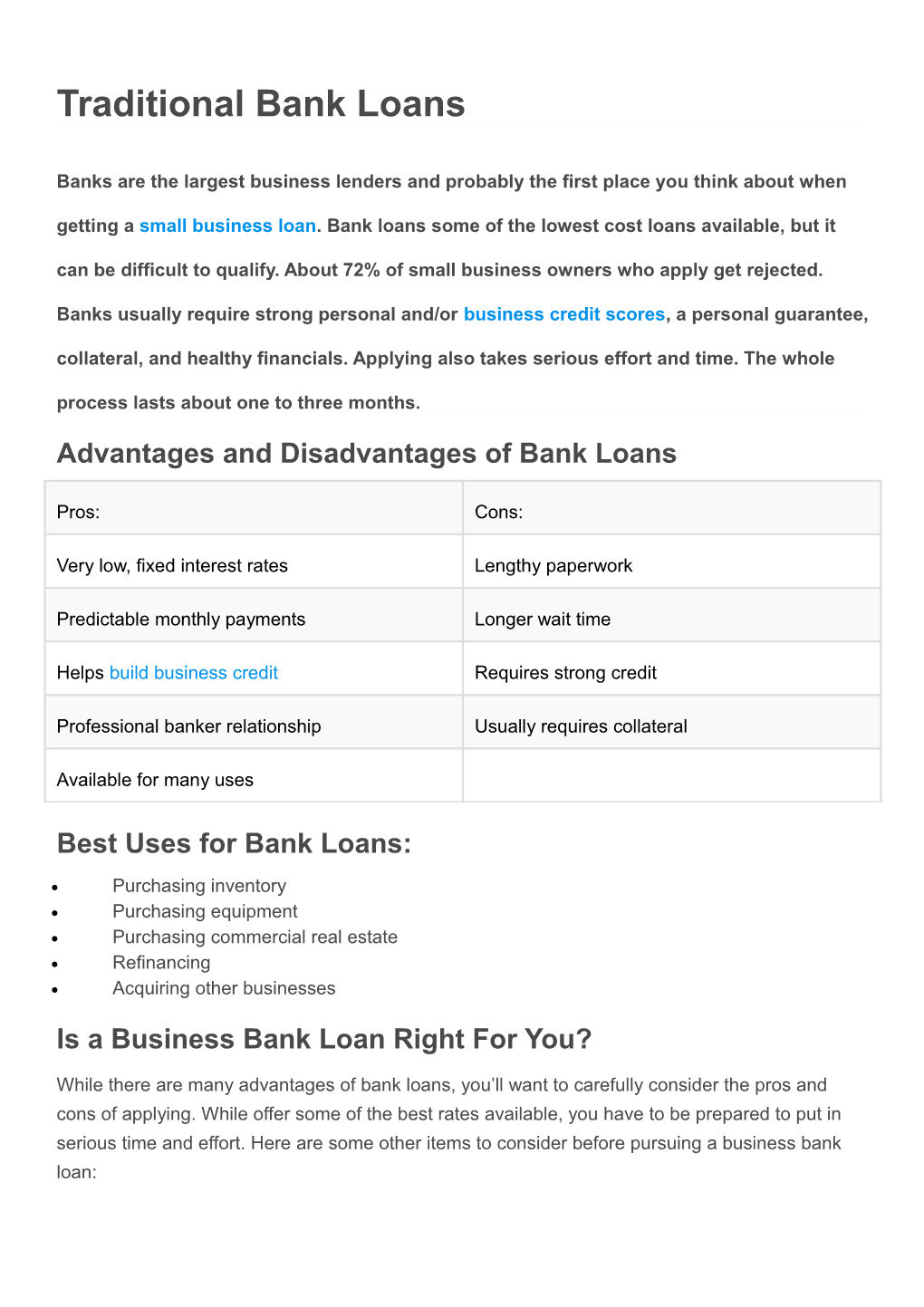

Advantages and Disadvantages of Bank Loans

Pros: / Cons:Very low, fixed interest rates / Lengthy paperwork

Predictable monthly payments / Longer wait time

Helps build business credit / Requires strong credit

Professional banker relationship / Usually requires collateral

Available for many uses

Best Uses for Bank Loans:

- Purchasing inventory

- Purchasing equipment

- Purchasing commercial real estate

- Refinancing

- Acquiring other businesses

Is a Business Bank Loan Right For You?

While there are many advantages of bank loans, you’ll want to carefully consider the pros and cons of applying. While offer some of the best rates available, you have to be prepared to put in serious time and effort. Here are some other items to consider before pursuing a business bank loan:

You’ll likely need excellent credit to qualify. If you have poor credit, it may be worth waiting to apply for a business bank loan and working on your credit scores first. This will put you in the best position to get through the application process with relatively little difficulty. (Check your personal and business credit scores for free with a Nav account.)

Banks want to see that your business is bringing in a healthy amount of cash flow. They will want to look at your business bank account statements to determine how if you have a large enough average daily balance to lend to, and to evaluate how much cash you’re bringing in in comparison to the amount of debt your business has. Separating your personal and business finances will help banks see what money your business is bringing in and boost your chances of getting a loan.

You’ll likely need to be an established business to work with a bank for business financing. Banks like to minimize their risk when it comes to business loans, so they may require you to have a couple years in business under your belt.

Banks will want to know the purpose of your loan. While bank loans are available for many uses, your lender will want to know how you are going to use the loan before extending you cash. One use of a bank loan, for example, is to finance equipment. Bank equipment loans are often easier to qualify for than other bank loans because you can use the equipment being financed as collateral for the loan.